Q3 2026 FORECAST

§1 — BOTTOM LINE UP FRONT

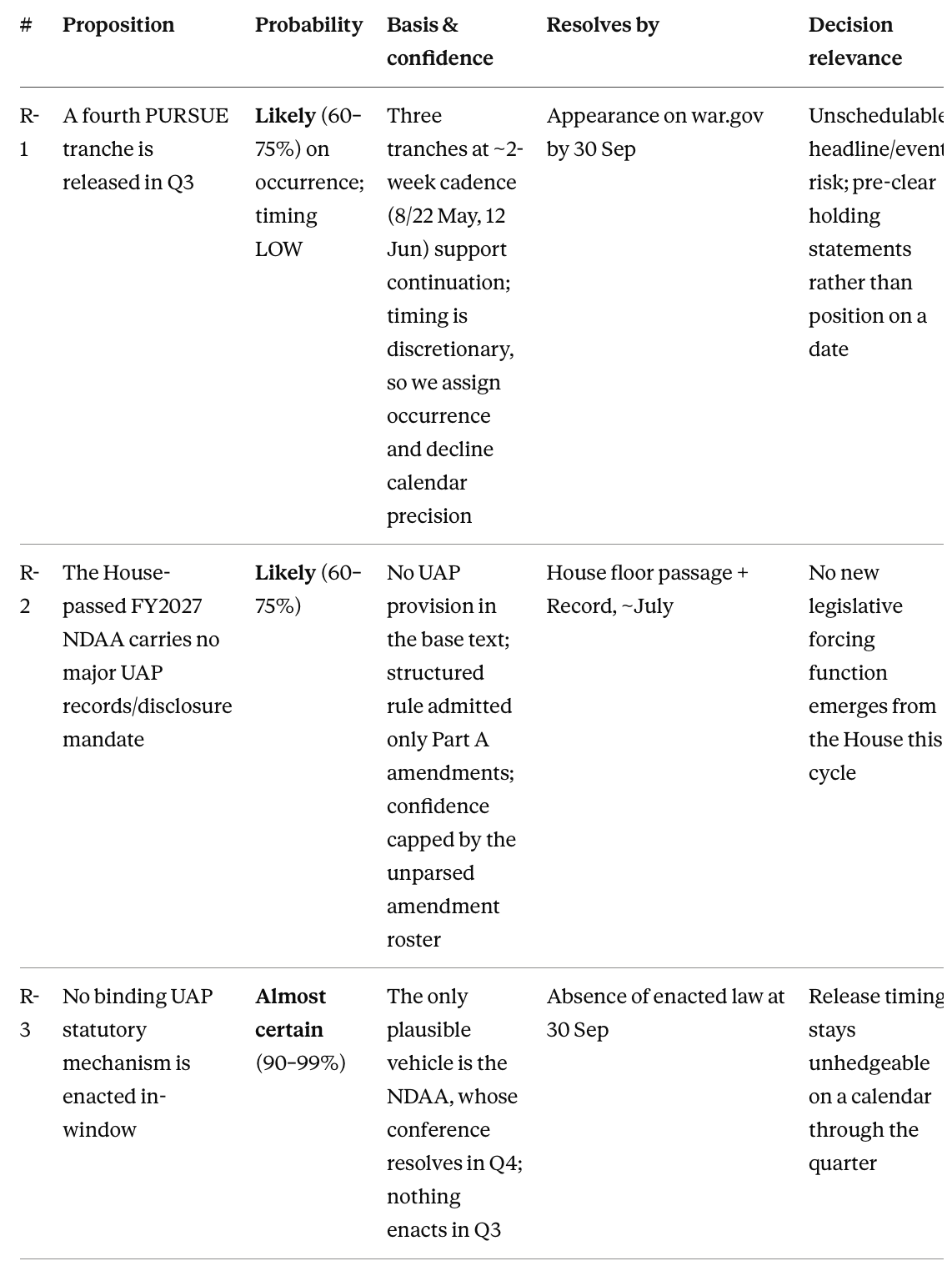

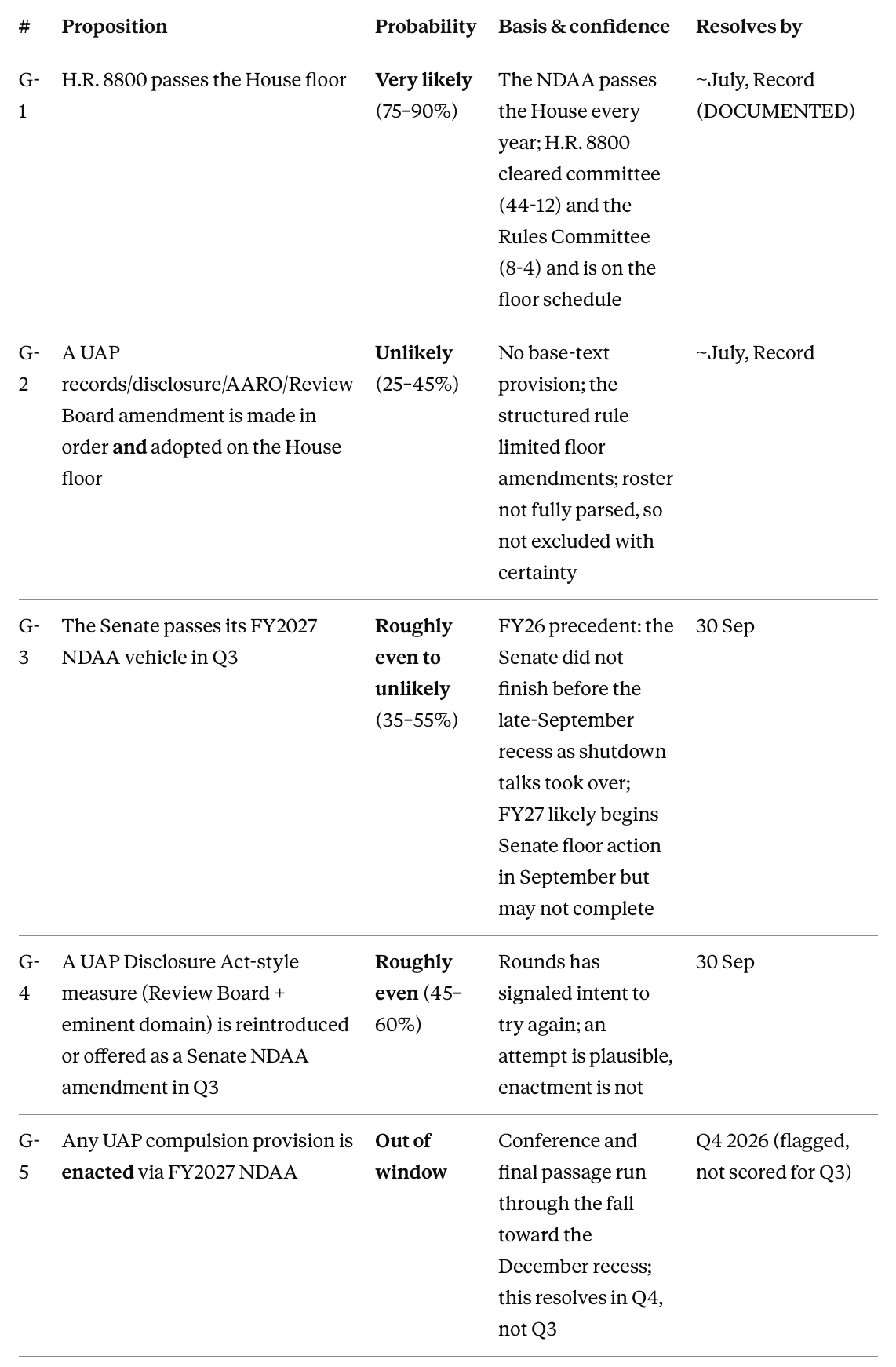

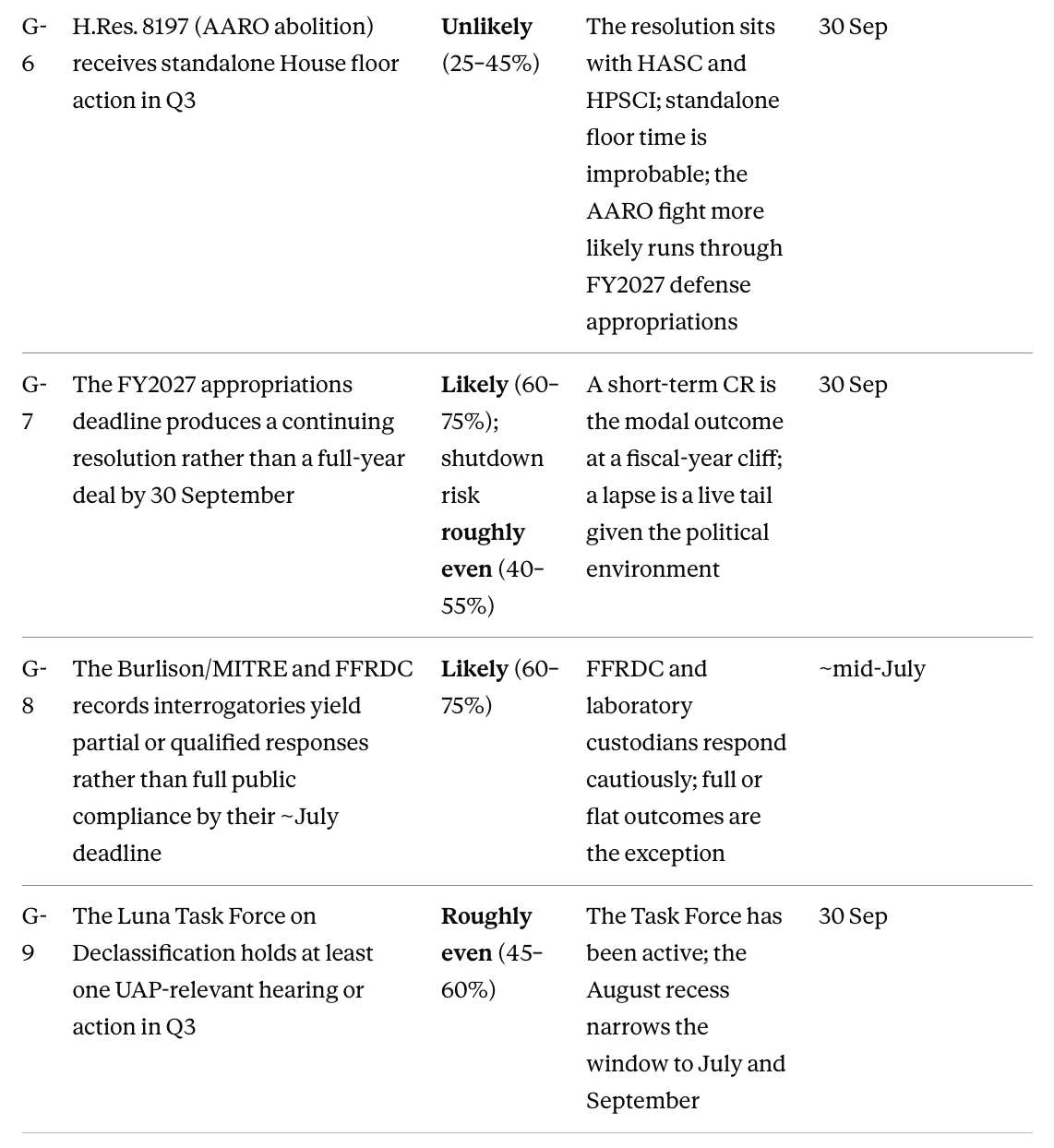

Q3 is a continuity quarter with a front-loaded decision and a back-loaded cliff. The single most consequential in-window event is the House floor vote on the FY2027 NDAA (H.R. 8800) in early-to-mid July, where we expect passage and no major UAP records or disclosure provision to survive. After that the legislative track goes quiet for the August district work period, then September is dominated by the 30 September fiscal-year-end appropriations cliff, which is where the fight over AARO's funding will actually play out. We hold that the disclosure apparatus remains executive-discretionary throughout, that no binding statutory forcing function is enacted in-window (the NDAA conference that could carry one resolves in Q4, not Q3), and that the two things most likely to actually move are a possible fourth PURSUE release and the House-floor disposition of any UAP amendment. The ODNI leadership transition and the AARO abolition fight stay contested but largely unresolved by quarter-end.

§2 — THE QUARTER'S CENTRAL JUDGMENT

The base case is continuity, and we argue up from it. Three things are most likely to move the picture, in descending order of probability: a fourth PURSUE tranche on the executive's discretionary schedule; the House-floor outcome on UAP NDAA amendments in July; and an escalation of the AARO abolition-or-defund fight through the September appropriations process. Everything else, including the binding-statute question and the permanent DNI succession, more likely advances than resolves within the quarter. The calendar itself is the dominant variable: a narrow legislative window in July, a dead zone in August, and a bandwidth-consuming shutdown fight in late September.

§3 — PROBABILITY VOCABULARY

Almost certain 90–99% · very likely 75–90% · likely 60–75% · roughly even 45–60% · unlikely 25–45% · very unlikely10–25% · remote 1–10%. Claim tiers used where they matter: DOCUMENTED, DOCUMENTED-AS-REPORTED, TESTIMONIAL, INFERRED, UNESTABLISHED. All forecast judgments are INFERRED by construction.

§4 — RISK-LED FORECAST (Spine 1)

For the board and the allocator. Standing convention: assessed intelligence with stated confidence, not investment, legal, or financial advice. Predictive and market calls default to LOW.

Counterparty and provenance flags for the quarter. A late-September shutdown or continuing-resolution fight could disrupt the cadence of records production and agency responsiveness, a process risk worth watching. Any "suspicious death" or sudden-whistleblower narratives that surface in Q3 should get a provenance and information-environment read before they are weighted; the fact of an event and the characterization of it travel separately. We continue to flag patent-stage or press-release "UAP-tech" claims as decision-anchors to reject absent independent replication.

§5 — GOVERNMENT-PROCESS FORECAST (Spine 2)

For the reader who needs the mechanics. The risk read above is downstream of this.

The calendar, stated plainly. July is the live legislative window and carries the House NDAA vote and the FFRDC deadlines. The August district work period is a legislative dead zone; expect little movement beyond any discretionary executive release. September returns the House to a floor dominated by the 30 September appropriations cliff, which is both the shutdown-risk event and the venue where AARO's funding is actually contested. The binding-disclosure question advances toward a Q4 conference but does not close in-quarter.

§6 — TECHNICAL CONVERGENCE: Q3 READ

The isolation null holds, and a single quarter is far too short to move it. We assess the probability of any genuine integration signal in Q3 — a single program coupling aneutronic fusion, high-field magnets, and an MHD or field-propulsion stage with replicated performance — as remote (1–10%), and more precisely we expect none. Any fusion milestone, magnet record, or propulsion announcement that appears in the quarter is generic progress in a separately funded field (an S0/S1 event), not evidence of convergence, and we explicitly decline to read any of it as bearing on UAP origins. We keep the three questions separate: is integration happening (no), is any reference architecture uniquely predictive (not assessed this quarter), does this bear on UAP origins (declined). Watch items that would not change the read but are worth logging: any aneutronic/p-B11 announcement, any REBCO field-strength record, any peer-reviewed propulsion claim. None would clear the bar in one quarter.

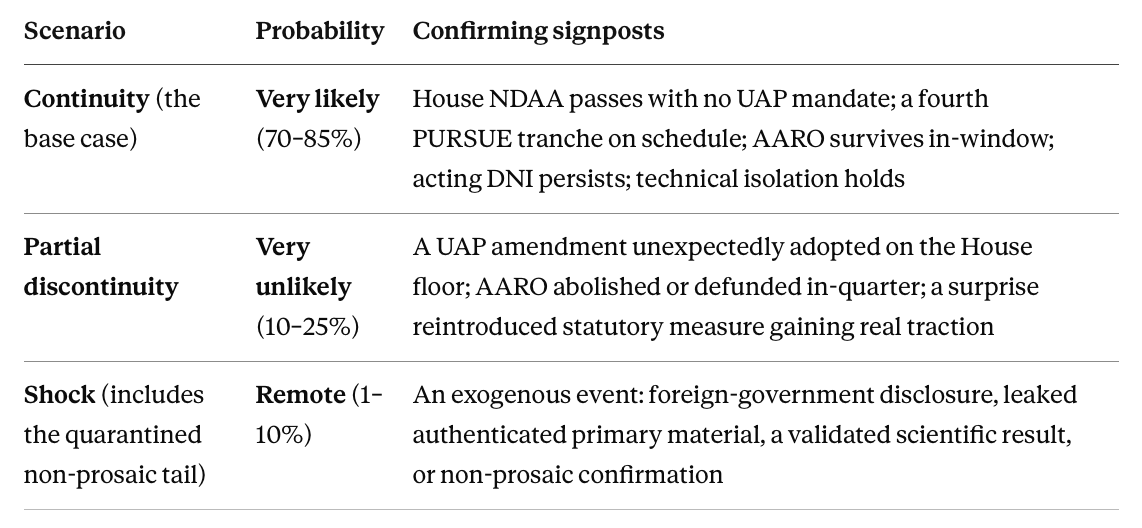

§7 — SCENARIO FLAGS (Q3)

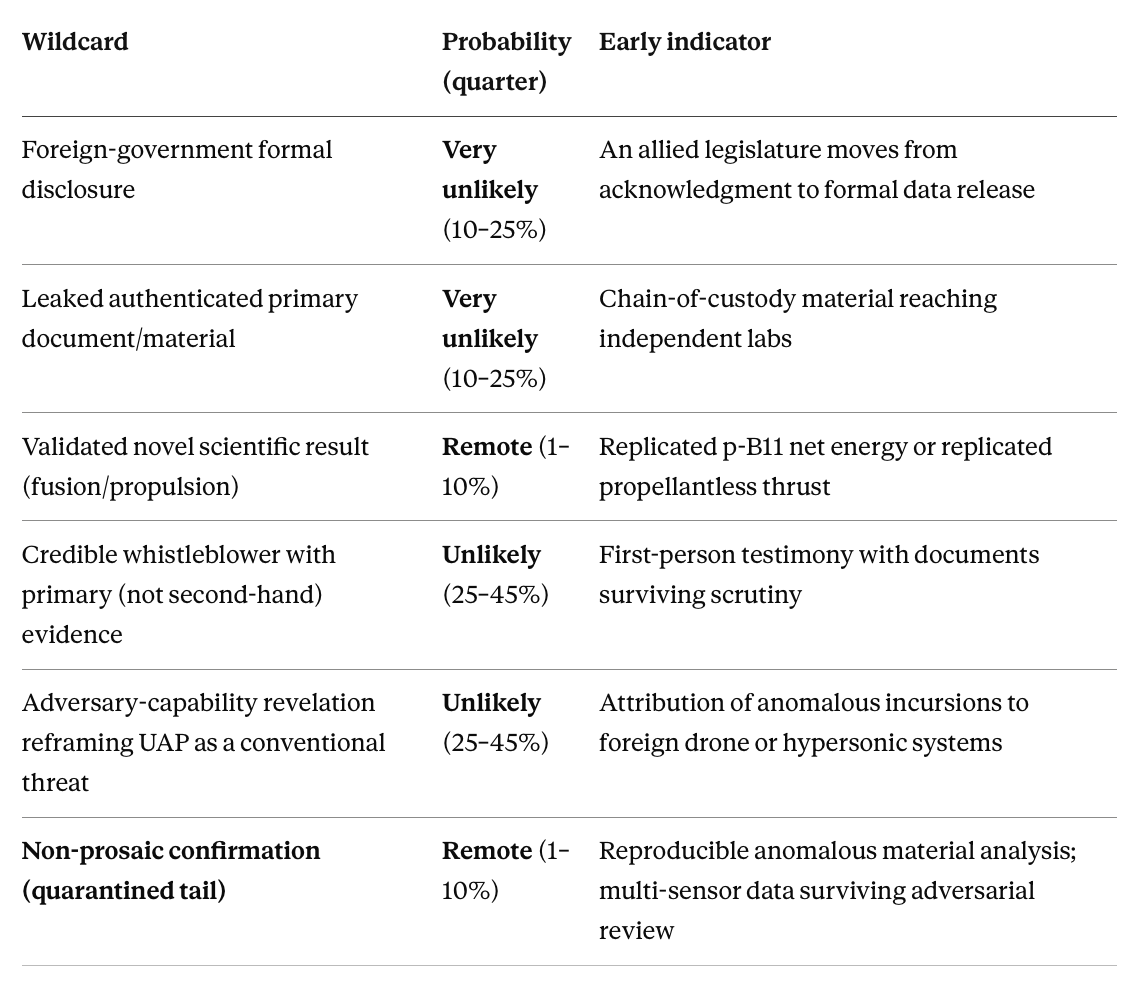

§8 — WILDCARDS / TAIL RISKS (Q3)

§9 — WHAT WOULD CHANGE THE FORECAST

Toward discontinuity: a UAP amendment adopted on the House floor; a reintroduced UAP Disclosure Act gaining Senate floor traction; AARO abolished or defunded through appropriations; a release shifting from unresolved cases to characterized capability; primary material surfacing outside the executive channel. Toward deeper continuity or reversion: a clean NDAA with no UAP language; a pause in the PURSUE cadence; a prolonged DNI vacancy; a September shutdown that consumes all oversight bandwidth and freezes the issue. Each is a dated, watchable signpost and would be reported as a new event, not folded silently into a revised view.

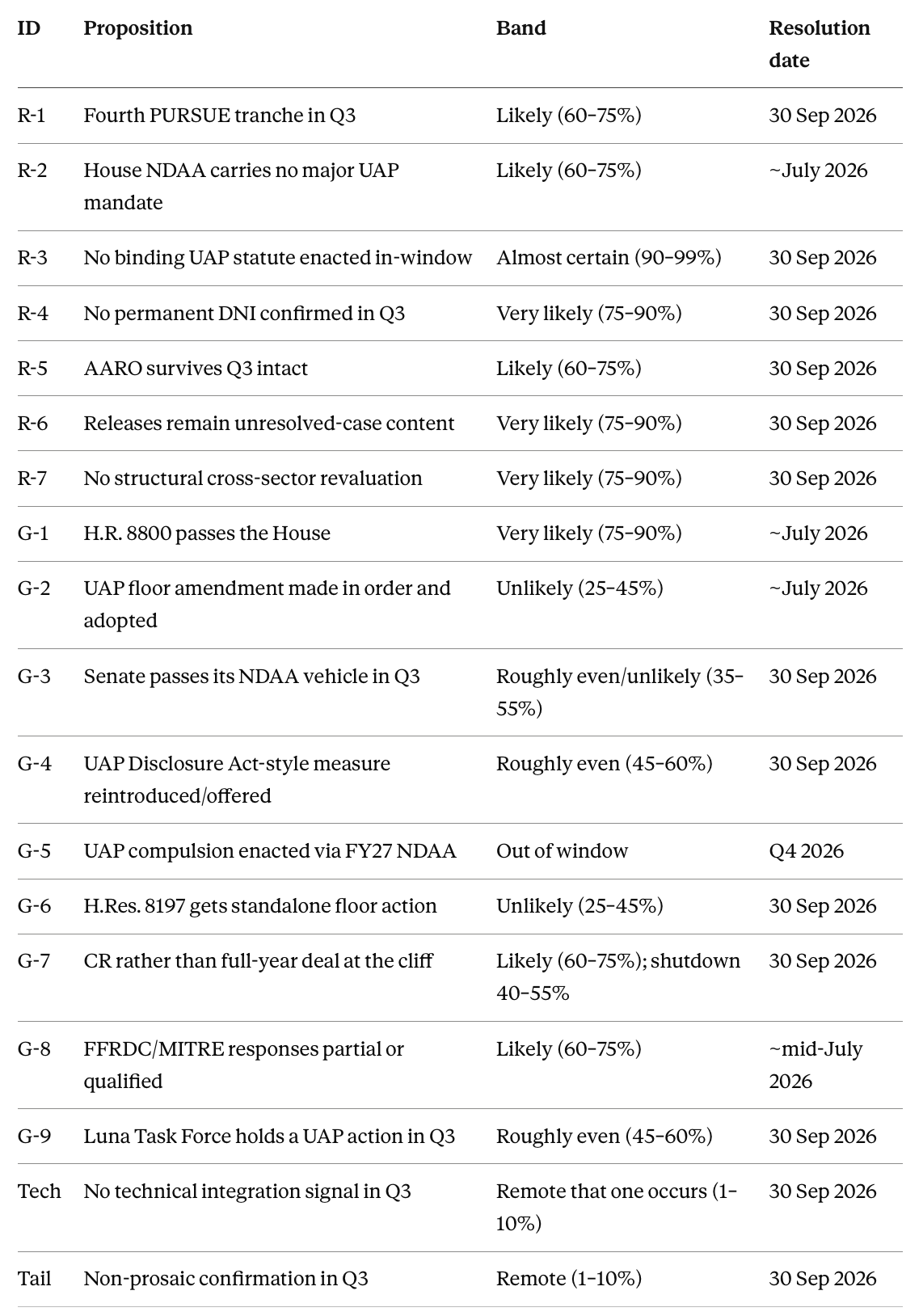

§10 — CALIBRATION LEDGER

This is a standalone Q3 product. Every proposition below is dated and gradable, and all but the explicitly out-of-window item resolve by 30 September 2026. We will score each at quarter-end as confirmed, disconfirmed, or unresolved, and publish realized hit-rate by probability band. Short-horizon forecasts are where calibration is most testable, and we will grade these.

§11 — CAVEATS

Continuity is the base case and the burden sits on anything that breaks it. Discretionary release timing is unschedulable on a calendar, so timing forecasts here carry low confidence while occurrence forecasts carry more. The binding-statute question advances toward a Q4 conference and does not resolve in Q3; readers should not expect closure on it this quarter. The technical-convergence read rests on the isolation finding and would be revised immediately by a distinctive-parameter result, which we do not expect in-window. The non-prosaic branch is quarantined at its remote band and is not load-bearing anywhere in this forecast. This is assessed forward judgment with stated confidence, not investment, legal, or financial advice, and all predictive and market-directional calls default to the lower end of the confidence they could support.